Can Lease-Purchase Arrangements Provide Another Pathway to Homeownership?

Maybe, but prospective buyers often navigate significant risks—and an unclear path—while renting

As policymakers look for ways to expand homeownership and help more homebuyers access credit, lease-purchase arrangements have received renewed attention not only from legislators, but from investors, prospective homebuyers, and nonprofit organizations. Proper use of these arrangements may help buyers who can’t quite qualify for a traditional mortgage or pull together the money they need for a down payment—but the approach can still pose risks for many potential purchasers.

A lease-purchase, also known as “rent-to-own” or “lease with option to purchase,” is a form of alternative home financing—a mechanism that potential homebuyers might consider when traditional credit is not immediately available to them. Under a lease-purchase arrangement, the property seller also acts as the landlord. The buyer rents the home as a tenant first, typically paying an up-front fee or down payment under an option contract to preserve the right to purchase the property within a set time period. Sometimes, during the rental period, the buyer is required to put aside some savings every month toward the home purchase. The seller transfers the deed to the buyer once the buyer obtains a mortgage to purchase the home.

A lease-purchase agreement consists of two components: the lease or rental agreement and a separate contract that allows the buyer to purchase the property within the rental period. If done properly, lease-purchase arrangements can help prospective buyers improve their credit scores, save for a down payment while living in a home of their choice, and ultimately become homeowners.

But many potential homeowners face challenges with the lease-purchase process; the outcomes and experiences do not always align with how these arrangements are advertised. What’s more, consumer experiences and outcomes with lease-purchases are hard to track down because of a lack of recording and data of such arrangements. The agreements work well for some potential buyers but others do not become homeowners when they conclude their rental agreements, sometimes because of home maintenance issues. Further, some may pay more than the median rental price in monthly payments or lose a portion of their savings put aside for the home purchase to fees if they decide to walk away from the arrangement.

Lease-purchases are different from land contracts, another alternative home-financing tool, although the two are often confused for one another. Lease-purchases appeal to buyers who may need more time to obtain a conventional mortgage or want to lock in a home price and a property in a competitive housing market. Other buyers with no access to traditional credit might instead opt for a land contract because of a quicker closing process and lower up-front expenses than a mortgage. But some land contract buyers and news articles have reported harmful outcomes that could deter others, such as evictions or loss of payments made. In comparison, some companies pitch lease-purchase arrangements as an innovative and easy path to homeownership because potential buyers can live in their “dream house” while setting aside a portion of their paycheck toward a home purchase down payment.

In fact, although lease-purchase agreement terms and laws differ from land contracts, the two mechanisms share similar pitfalls, such as unclear consumer protections for the buyer, unclear responsibilities regarding taxes and maintenance, a lack of recording requirements, and little data or transparency of ownership.

Market embraces wave of business players

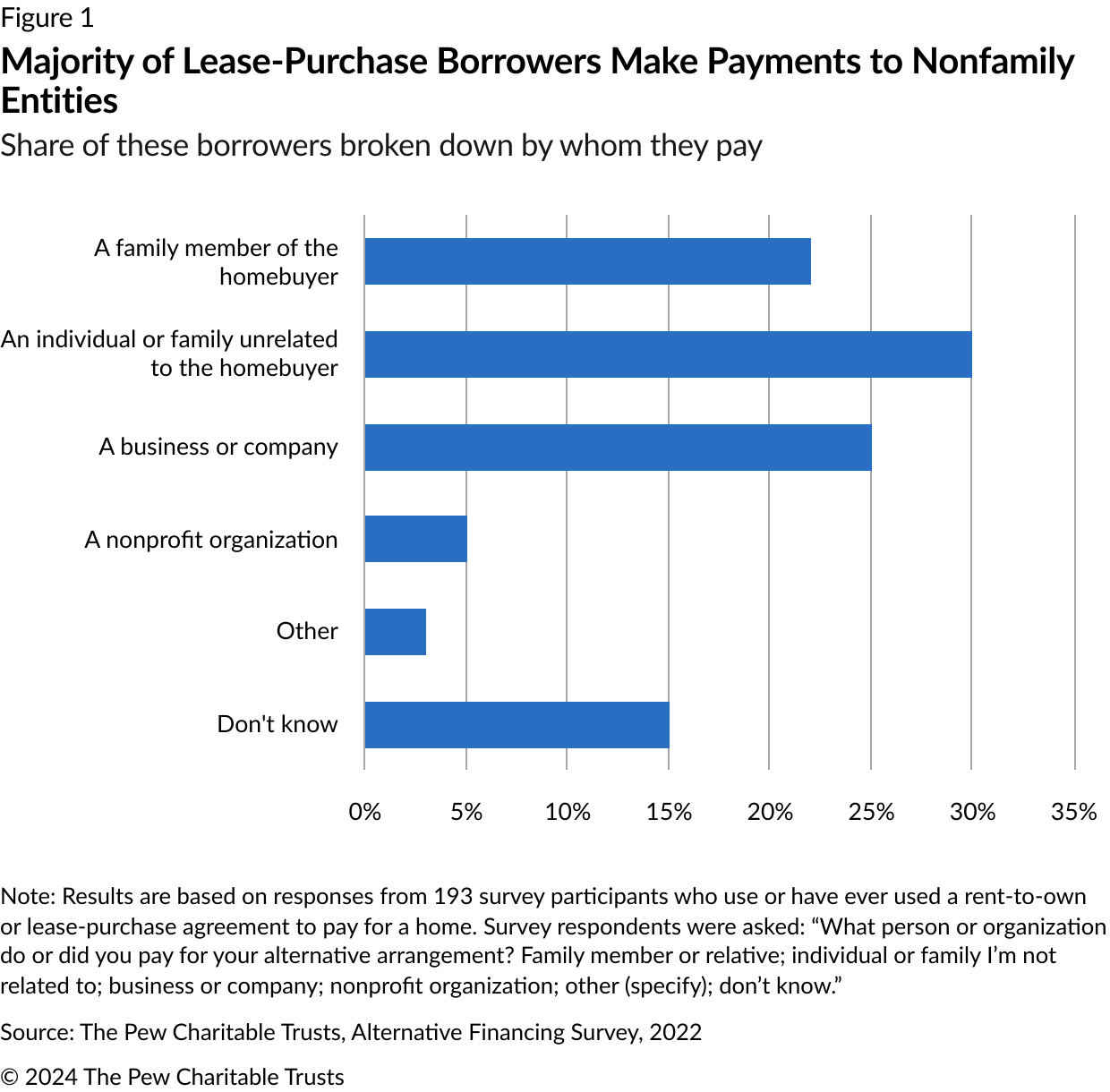

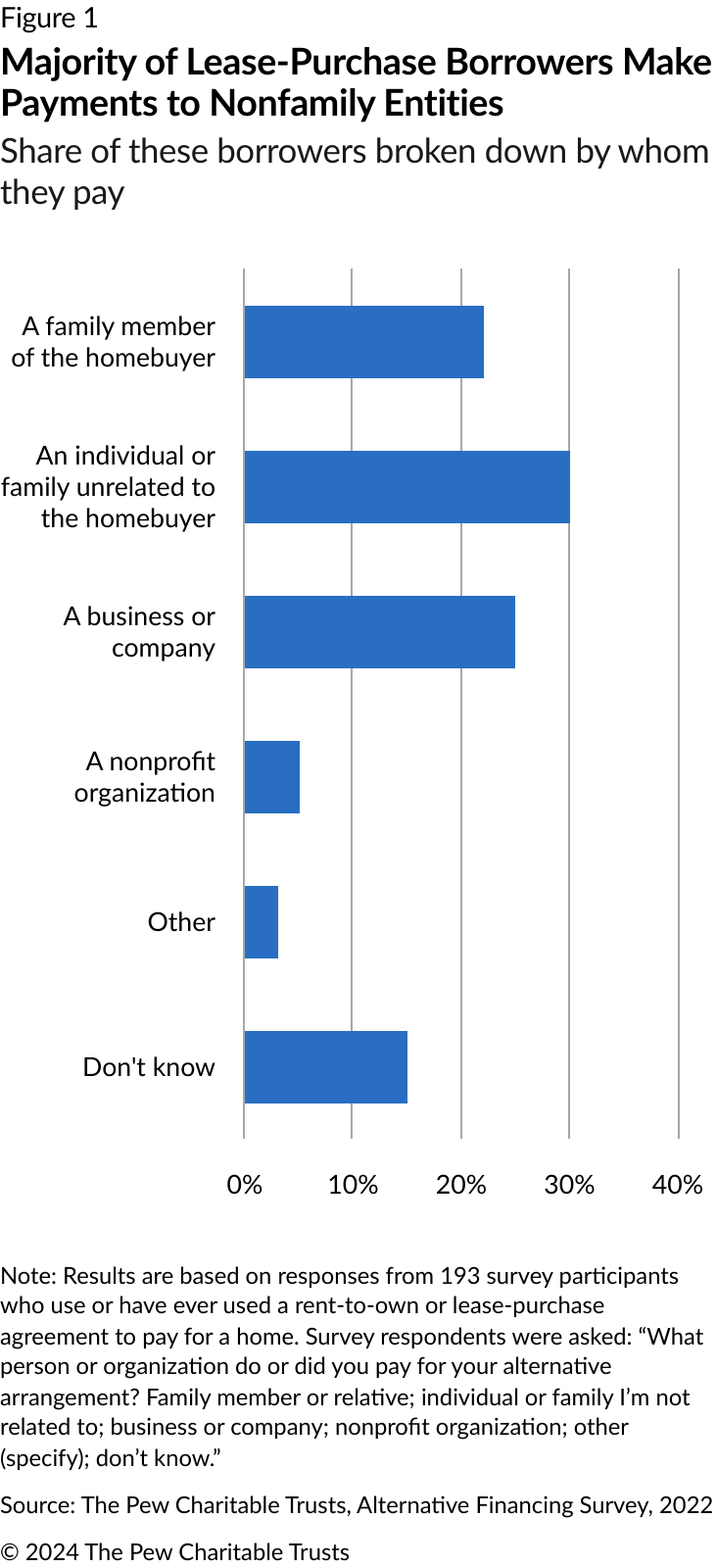

According to The Pew Charitable Trusts’ nationally representative surveys about alternative financing in 2021 and 2022, about 2.4 million adults living in 1.2 million U.S. households use lease-purchase agreements. Based on the estimated number and median value of currently used lease-purchase arrangements in the Pew surveys, these agreements have an estimated total value of $196 billion. In recent years, financial technology (fintech) companies and other investors have turned to the lease-purchase market with a focus on buying single-family homes. According to Pew’s survey on alternative financing in 2022, about 60% of these lease-purchase borrowers make payments to nonrelatives, companies, or organizations they do not know, as opposed to family or friends. (Figure 1.)

Still, such agreements are not regularly recorded or tracked by any public or private sources. And lawsuits against some lease-purchase players over evictions and home repairs highlight the complexities and potential pitfalls of these arrangements.

Gaps in state laws leave lease-purchase borrowers in limbo

An estimated 6% of home borrowers in the United States have used lease-purchases, but state laws don’t treat such arrangements uniformly.

And the distinct two-part structure of lease-purchase arrangements often confuses buyers about applicable consumer protections. For example, the sellers, usually also the landlords, are generally responsible for keeping the property safe and livable for tenants. During the rental period, lease-purchase agreements tend to be governed by state landlord-tenant laws. Once prospective buyers conclude their rental period, they must decide if they want to exercise their option to purchase the home—typically with a mortgage—which would grant them state and federal mortgage protections after the purchase.

However, few state or local laws govern the option contract in a lease-purchase arrangement—the transitional stage until the renter formally purchases the home using a home loan and becomes a homeowner. Sellers often privately hold the option contracts during the arrangement and do not publicly record them. The contract may stipulate the home price, any additional fees, and buyer’s responsibilities until the home is secured with a mortgage. To complicate matters more, agreements drafted by companies can differ significantly from those offered by individuals.

Upcoming Pew research on lease-purchases

To get a fuller picture of the lease-purchase landscape, Pew has conducted nationally representative surveys and in-depth interviews and commissioned a review of state laws. Future Pew publications will examine the outcomes of these arrangements, analyze lease-purchase company business practices, and develop policy recommendations to expand consumer protections for lease-purchase homebuyers.

The results of this research should provide a more comprehensive understanding of these agreements and their role in the housing market and may help guide better policies and practices to support potential homeowners.

Methodology

Pew estimated the total number of active lease-purchase agreements based on findings of its 2021 nationally representative survey—0.93% of U.S. adults were actively using a lease purchase to finance a home purchase at that time. Then, given that lease-purchase buyers’ average household size is comparable to that of the country as a whole, Pew applied that percentage to the total number of households in the U.S. in 2022. That yielded an estimate of 2.4 million households that were actively using a lease-purchase agreement. Using this survey’s margin of error for the subgroup, the true number of active lease purchases could be anywhere from 498,000 to 4.3 million. Although the relative scarcity of lease purchases makes this estimate less precise, it is nevertheless probable since lease purchase are not publicly recorded and are therefore invisible to federal, state, and local governments.

Linlin Liang is a principal associate and Dennis Su is an associate with The Pew Charitable Trusts’ housing policy initiative.

ADDITIONAL RESOURCES

Article

Article