Land Contracts Pose 5 Major Risks for Homebuyers

Strengthening consumer protections can help avoid the worst outcomes

Overview

As of 2022, about 1.4 million Americans were using a form of alternative financing known as land contracts for their home purchases.1 In a land contract—also called a contract for deed or a land installment contract—the home seller extends financing directly to the buyer without the involvement of a third-party lender. The buyer then makes regular payments over an agreed-upon period, gaining full legal ownership of the property only after making the final payment.

Homebuyers choose land contracts for various reasons. Some buyers prefer land contracts because they close more quickly and can have lower up-front costs than mortgages. Others believe they cannot qualify for a mortgage. And still others find that mortgages are not readily available for the home or in the community where they hope to live. However, land contracts also carry significant risks for homebuyers, largely because they lack the basic consumer protections that are standard for mortgages.2 Few national lending laws apply to these arrangements and, even when they do, enforcement is weak.3 Furthermore, less than half of states have laws governing land contracts, and these laws are weaker and less uniform than the laws that apply to mortgages.4

To better understand the risks of land contracts, The Pew Charitable Trusts interviewed 55 legal aid professionals throughout the country with experience assisting homebuyers who have used these arrangements. The findings of those conversations largely aligned with the results of a Pew-commissioned nationally representative survey of 282 land contract homebuyers conducted in 2022. (See the methodology for more information.) Together, the interviews and survey reveal five main risks posed by today’s land contract market:

- Lack of transparency and clear written terms: Land contracts often are not publicly recorded— that is, filed with the city or county—making the transaction invisible to local governments. Because most state laws do not require standardized recording of land contract transactions, sellers may draft contracts that lack basic information about payment amounts, contract terms, and ownership responsibilities—and some may not provide buyers with any type of written contract.

- Forfeiture of down payment and home equity: Land contract homebuyers often lose their entire financial investment if they fall behind on their monthly payments because, unlike mortgage holders, land contract homebuyers often go through eviction proceedings rather than more buyer-friendly foreclosure processes. Homebuyers who are evicted forfeit the right to their down payment, principal payments, and home appreciation, often ending up in a worse financial position than they were in before they started their arrangement.

- Inclusion of balloon payments: Many land contracts include large, one-time payments toward the end of the contract term that impose additional financial burdens on homebuyers working to repay their land contracts and increase the risk that buyers will lose their homes and investments.

- Unsafe or uninhabitable homes: Many homes financed with land contracts have major structural problems or other undisclosed repair needs that make them unsafe or unhealthy to live in. In some land contract transactions, sellers place the responsibility for remediating these habitability issues on buyers. These additional costs can be high, can make repayment more difficult for buyers, and typically do not provide equity to buyers who never take full ownership of the property.

- Payment of property taxes without full ownership: Land contract sellers often require homebuyers to pay property taxes and home insurance premiums before the buyer has full legal ownership of, also known as having title to, the home. This can be financially burdensome for homebuyers, especially when the property has a backlog of unpaid taxes—a common condition when land contract sellers acquire properties out of foreclosure.

Despite the risks, 87% of respondents to Pew’s survey who had either left or repaid a land contract rated their experience as somewhat or extremely positive, 88% said that they eventually achieved homeownership, and about 56% reported that they still own their land contract-financed property. These outcomes help explain why, rather than seeking prohibitions on land contracts, many of the legal aid attorneys that Pew interviewed want stronger protections to ensure clearer, safer, and more transparent agreements that enable buyers to achieve homeownership.

Pew’s research indicates that policymakers seeking to improve outcomes for land contract homebuyers should focus on improving the availability of small mortgages (those under $150,000), which offer stronger protections than land contracts. Additionally, policymakers can take steps to improve land contracts by establishing baseline protections to address key risks. In particular, land contracts should be publicly recorded, enable borrowers to retain their investments in the home, not require balloon payments, and clearly enumerate the buyer’s and seller’s respective responsibilities during the contract term. Together, these changes would help ensure that homebuyers can achieve and sustain affordable homeownership.

Methodology

To better understand the experiences of land contract homebuyers, Pew conducted two types of original research: a first-of-its-kind, nationally representative survey exploring the attitudes and opinions of land contract homebuyers and a series of in-depth interviews with legal aid professionals nationwide who have experience working with land contract homebuyers.

Pew’s survey of alternative financing borrowers was conducted from April 2022 to May 2022 and yielded 1,317 responses from adults ages 18 and over, of which 282 currently or previously used a land contract. (See the separate Appendix for the full survey results.) The survey also asked about other forms of alternative financing, including seller-financed mortgages, rent-to-own (also called lease-purchase) agreements, and personal property loans, but those financing types were excluded from this analysis.

From February 2021 to September 2022, Pew researchers conducted 55 interviews with legal aid attorneys in 29 states.5 Legal aid attorneys were qualified to participate if they had supported clients who had used alternative home financing to purchase their homes, including seller-financed mortgages, land contracts, lease-purchase agreements, and personal property loans. Findings from the interviews are based on convenience sampling and are not intended to be representative of legal aid attorneys or their clients.

Land contracts lack transparency and clear written terms

Mortgage-financed home sales are almost always publicly recorded because state law requires it or because lenders want to protect their financial interest in the property. However, homes purchased with a land contract do not involve a lender, and only about a dozen states require that land contracts be publicly recorded.6 Absent statutory requirements, recording is typically at seller discretion, and habits differ geographically. In some states without requirements, sellers tend to record their arrangements anyway for various reasons, including case law or a longstanding culture of recording.7 Additionally, some states do not record land contract transactions under any circumstances.

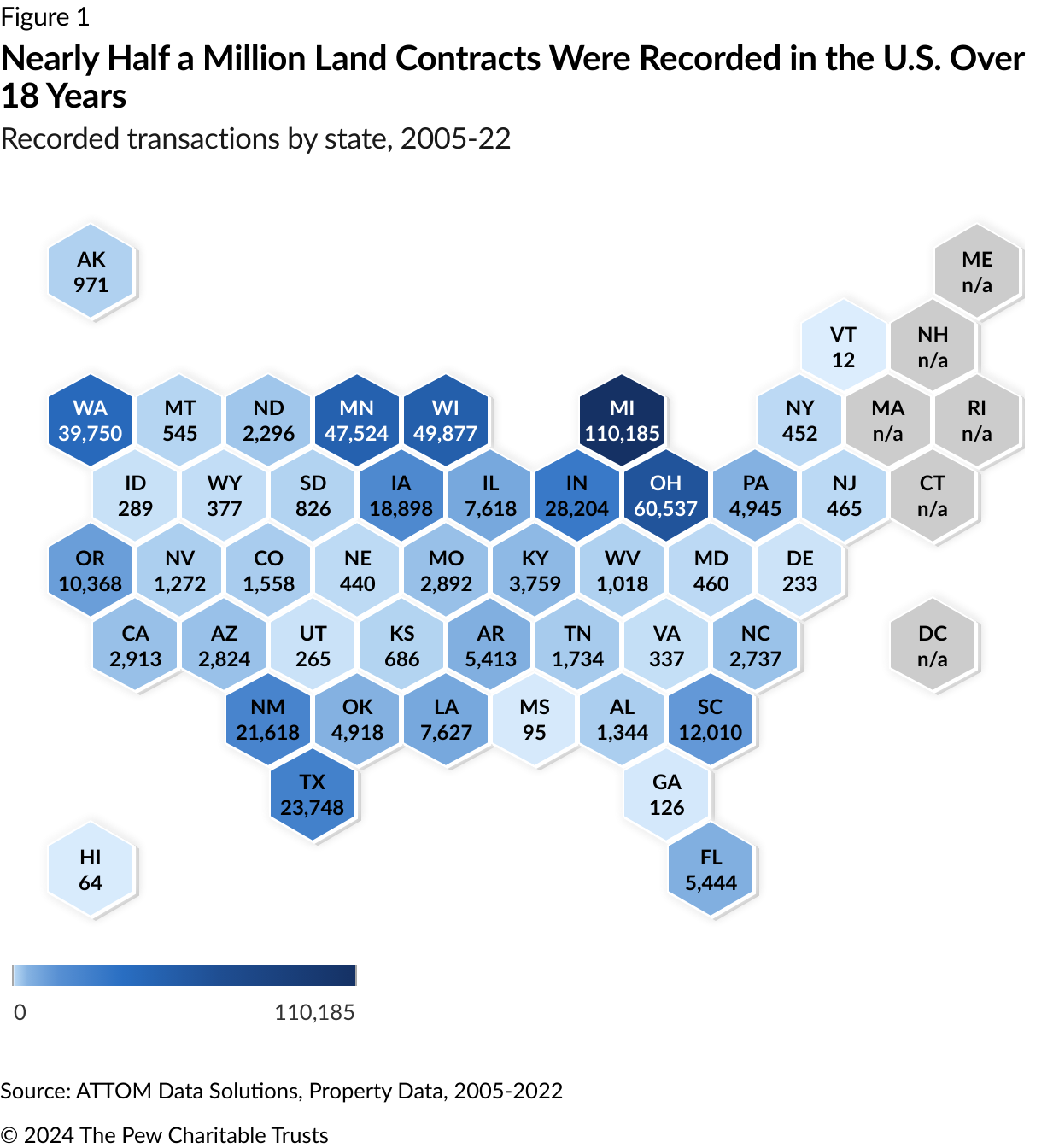

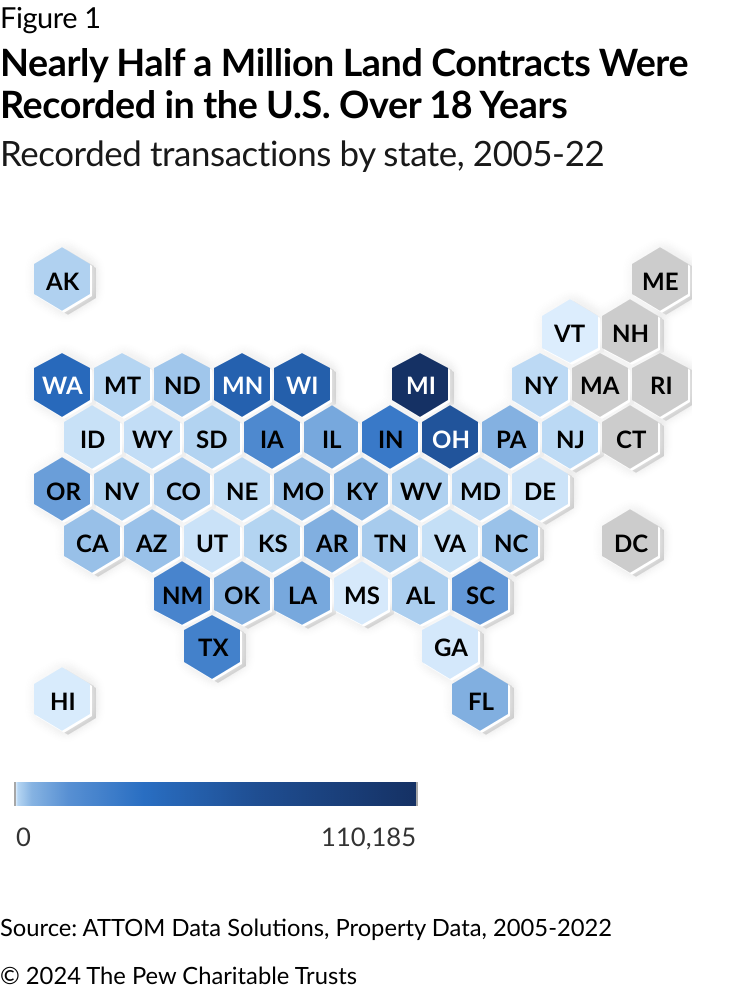

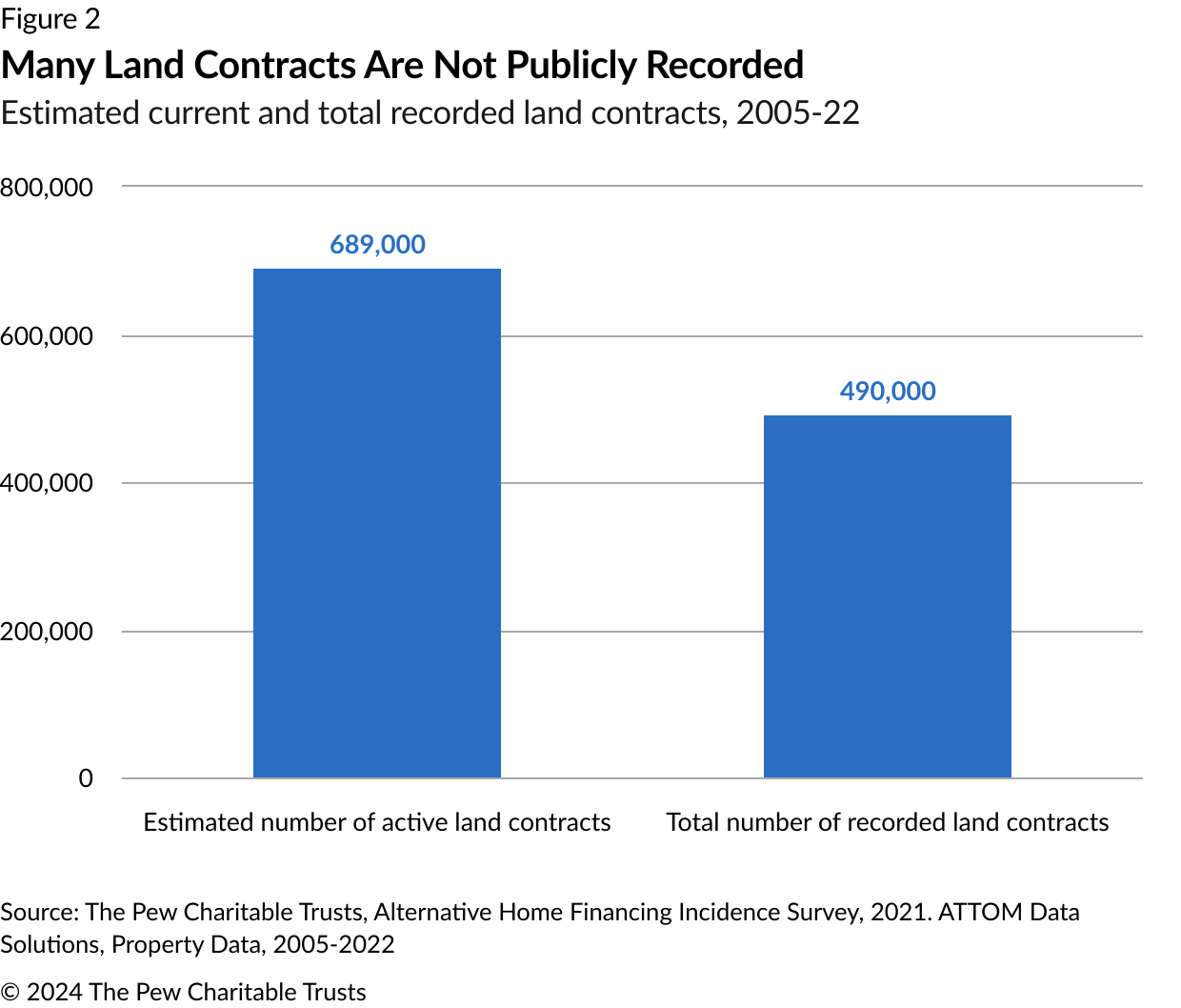

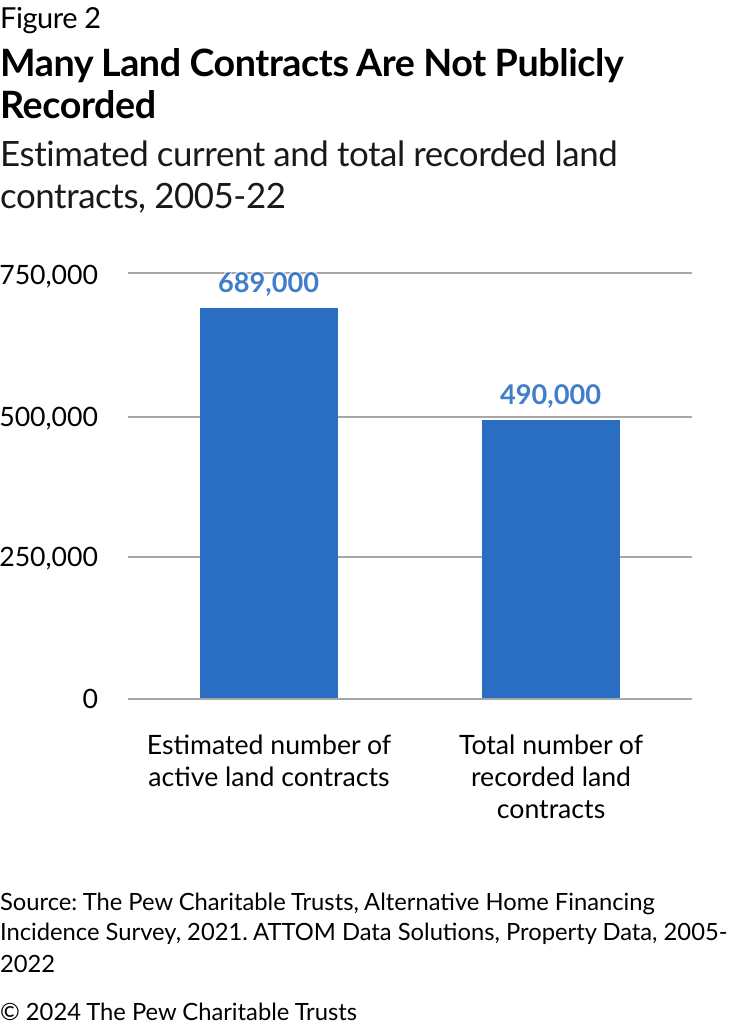

In Pew’s survey, 78% of respondents said their land contracts were recorded, 10% said they were not, and 12% did not know. Further, Pew analyzed property records data and found that about 490,000 land contracts were recorded across the country from 2005 to 2022, of which 383,000 covered residential properties. (See Figure 1.)

However, Pew’s survey results indicate that far more households—about 689,000—currently use a land contract.8 (See Figure 2.)

Because sellers often are not required to publicly record land contract transactions, some choose not to provide buyers with written contracts that formally document each party’s commitments. In Pew’s survey, 8% of respondents said that they did not receive or were not sure they received a written contract. Further, respondents whose land contracts were not publicly recorded were six times as likely to have never received a written agreement as those whose contracts were recorded. These findings suggest that improved public recording could help homebuyers better understand their contract terms, such as interest rates, payment terms, amortization schedules, and outstanding balances.

Unrecorded land contracts also put homebuyers’ financial interest in a property at risk. Without public documentation of the transaction, land contract buyers may be unable to prove their ownership of a property, which can prevent them from accessing government programs that benefit homeowners, such as a homestead tax exemption, and possibly make them ineligible for title insurance, which protects buyers in cases of contested property ownership.

Buyers often lose down payments and other investments

In theory, land contract homebuyers share ownership of their property with the seller for the duration of the contract and have the right to benefit from their home’s appreciation. Yet ambiguous state laws and spotty land contract recording practices mean that in practice, homebuyers are at risk of losing their payments, accrued equity, and other investments in the home until they make their final payment and take title to the property. Pew’s survey found that many buyers who terminated their arrangements before making the last payment lost their entire investment, and some even owed more than they did at the start.

Further, in Pew’s interviews, many legal aid attorneys said that state laws do not provide guidance on whether land contract homebuyers should go through eviction or foreclosure proceedings. As a result, sellers often choose eviction, which is faster and usually benefits the seller financially.9 But for buyers, eviction proceedings present several challenges compared with foreclosure: Buyers who are evicted can be put out of their home within weeks of falling behind on their payments, rather than months, and they do not have the opportunity to catch up on missed payments (a process known as “curing”), retain the equity they have built, or sell the house to recoup some of their investment.10

Land contracts often require balloon payments

Some land contracts include balloon payments: large, one-time payments due near the end of a loan’s term. In the early 2000s, mortgage lenders often used balloon payments to extract additional fees and penalties from borrowers.11 But after the Great Recession of 2007 to 2009, many of those borrowers defaulted, prompting the federal government to restrict the use of balloon payments in mortgage lending.12 As of 2022, less than 1% of all mortgages included balloon payments.13 In contrast, 14% of Pew’s survey respondents said that their land contract listed or otherwise disclosed a balloon payment.

Several of the legal aid attorneys whom Pew interviewed said that among homebuyers who had struggled in their land contracts, many were contractually required to make balloon payments. Some interviewees also reported that sellers misled buyers to believe that they could get other financing to cover their balloon payments but that in practice such financing is rarely available. Without cash or financing to make balloon payments, some borrowers are unable to make all their required payments, putting them at risk of losing their home and their investment.

Many land contract properties need major repairs and renovations

Many land contract properties are in significant disrepair, requiring extensive and costly upgrades in order to be made habitable. Although some buyers intentionally seek out lower-cost “fixer-upper” homes that are unlikely to qualify for mortgages, others unknowingly buy compromised homes that can threaten their health and need major repairs to meet minimum local safety codes.

The lack of a comprehensive national regulatory standard with strong, uniform protections on land contracts exacerbates this issue. As of this writing, Virginia is the only state with a law that sets criteria for the habitability of land contract properties, requiring that they meet the same standards as rental properties in the state.14 In interviews, some legal aid attorneys commented on the varying quality of homes bought with land contracts—and of the language in some contracts regarding habitability—in their states:

- Georgia: Some land contracts contain language requiring the buyer to “bring the home into habitable condition” within a certain time frame.

- Alabama: Certain land contract properties “should not even be sold” because they would not pass a standard home inspection.

- South Carolina: Many land contract homes were “not in acceptable condition,” and buyers were often responsible for fixing the home’s defects.

Survey data confirms these observations. Among land contract buyers, 25% reported that their property needed major repairs or renovations, although many knew about the issues before purchasing the home. Further, nearly half of land contract buyers reported that they did not receive a home inspection—a common process for home transactions involving a mortgage—which could mean these buyers were not aware of some problems before moving into their homes.

When land contract properties need repair, some buyers pay for the upgrades themselves, even though they may not have clear ownership of the home or rights to the equity generated by those improvements. Some land contract buyers can incur thousands of dollars in expenses fixing up their home, only to later lose that investment if they miss a payment.15 These improvements add to the cost of a land contract property and can strain buyers’ budgets and threaten their ability to make the regular payments.

Most land contract homebuyers pay property taxes, even when their name is not on the deed

Local property taxes are typically the responsibility of the homeowner. But in the case of land contracts, ownership can be ambiguous, and sellers may shift the responsibility for property tax payments to homebuyers, often without clearly disclosing it in the contract. In Pew’s survey, 73% of land contract homebuyers reported being responsible for the property taxes on their homes. Those tax payments can increase buyers’ housing costs by thousands of dollars a year, potentially compromising homebuyers’ ability to balance their budgets and stay current on housing payments. Further, unrecorded land contracts are often ineligible for common property tax reduction programs, such as a homestead exemption for owner-occupied properties.16

Moreover, land contract homebuyers may also inherit unpaid property taxes that accrued on the home before they entered into their arrangements. One way in which many land contract sellers acquire properties is through foreclosure sales—bulk sales of homes that have delinquent property taxes or other encumbrances, which then become the responsibility of the new owner. Land contract sellers, however, sometimes neglect these obligations and offload them onto the buyer, according to legal aid attorneys in Georgia, Kentucky, and Michigan. Although some buyers voluntarily enter into agreements that require them to pay back taxes and fees, attorneys noted that others are not aware of their home’s delinquent taxes until a bill arrives in the mail.

Policymakers can help protect land contract homebuyers

State and federal policymakers seeking to improve the experiences of land contract homebuyers should focus on simultaneously expanding access to mortgage credit and strengthening the consumer protections for land contracts. Some key measures to consider include:

Require that land contracts be publicly recorded. States should mandate that all land contracts be recorded with the local recorder of deeds to create proof of a homebuyer’s ownership status and responsibilities, make it easier to ascertain whether a property has active liens, and ensure that these arrangements are accessible to courts and governments. Currently, 13 states require that land contracts be publicly recorded, but enforcement of these laws varies across jurisdictions. Policies that encourage recording would help to strengthen protections for buyers and sellers and provide housing advocates, researchers, policymakers, and others with better data on how people finance low-cost homes.

Improve disclosure of terms and void balloon payments. Require land contract sellers to provide buyers with written contracts that fully disclose all terms, including the sale price, payment schedule, interest rate, prepayment penalties, existing liens on the property, and which party is responsible for paying for home repairs and property taxes. Policymakers should also void predatory terms and fees, such as balloon payments, which hurt buyers’ ability to pay off the contract and obtain the deed to the property.

Clarify the definition of and expand protections for land contract homebuyers. In many instances, state laws are unclear about whether land contract homebuyers should be treated as homeowners or tenants. State policymakers should review their statutes and make explicit whether land contract homebuyers are covered by laws applicable to homeowners, which would extend them homeowner protections and enable them to retain their equity, or by laws applicable to renters, which would relieve them of any responsibility for home repairs and property taxes—and place those obligations on the landlord/seller—until they acquire the deed to the property.

Expand access to small mortgages. Most land contracts are used to purchase properties valued at less than $150,000, a threshold below which obtaining a mortgage can be difficult.17 By taking steps to expand the supply of small mortgages, policymakers can ensure that borrowers are not forced to use a land contract because of a lack of available financing options. Small mortgages are always recorded, offer borrowers standard homeowner protections, rarely contain balloon payments, and preserve a borrower’s financial investment, making them a superior option to land contracts in most cases.

Conclusion

Homebuyers who use land contracts to finance the purchase of a home are exposed to risks not faced by buyers who use mortgages. Although many land contract buyers successfully navigate these risks and achieve homeownership, others end up worse off than they began. Lawmakers can act to reduce negative buyer experiences by strengthening protections and enacting policies to address the five main risks of land contracts. By mandating that land contracts be publicly recorded, eliminating harmful contract terms and practices, and expanding access to small mortgages, state leaders can enhance the safety of these alternative financing arrangements and help homebuyers retain their equity and achieve homeownership.

External reviewers

This brief benefited from the valuable insights of Elizabeth Blosser and Steve Gottheim of the American Land Title Association and Evy Zwiebach of Enterprise Community Partners. Although they reviewed drafts of the brief, neither they nor their institutions necessarily endorse the findings or conclusions.

Acknowledgments

This brief was researched and written by Pew staff members Adam Staveski, Linlin Liang, and Tara Roche. The project team thanks current and former colleagues Chase Hatchett, Gabriel Kravitz, Sarah Spell, Jacqueline Uy, Paul Durbin, Jennifer V. Doctors, Carol Hutchinson, Omar Antonio Martínez, Chelsie Pennello, and Mark Wolff for providing communications, creative, editorial, and research support for this work.

Endnotes

- The Pew Charitable Trusts, “Millions of Americans Have Used Risky Financing Arrangements to Buy Homes,” 2022, https://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2022/04/millions-of-americans-have-used-risky-financing-arrangements-to-buy-homes.

- Ann Carpenter, Taz George, and Lisa Nelson, “The American Dream or Just an Illusion? Understanding Land Contract Trends in the Midwest Pre- and Post-Crisis,” Joint Center for Housing Studies of Harvard University, 2019, https://www.jchs.harvard.edu/sites/default/files/media/imp/harvard_jchs_housing_tenure_symposium_carpenter_george_nelson.pdf; Heather K. Way and Lucy Wood, “Contracts for Deed: Charting Risks and New Paths for Advocacy,” Journal of Affordable Housing & Community Development Law 23, no. 1 (2014): 37-48, https://www.jstor.org/stable/26408134?seq=1.

- Jeremiah Battle Jr. et al., “Toxic Transactions: How Land Installment Contracts Once Again Threaten Communities of Color,” National Consumer Law Center, 2016, https://nclc.org/images/pdf/pr-reports/report-land-contracts.pdf; “Real Estate Settlement Procedures Act (RESPA) Examination Procedures,” Consumer Financial Protection Bureau, 2018, https://www.consumerfinance.gov/compliance/supervision-examinations/real-estate-settlement-procedures-act-respa-examination-procedures/.

- National Consumer Law Center, “Summary of State Land Contract Statutes,” 2021, https://www.pewtrusts.org/en/research-and-analysis/white-papers/2022/02/less-than-half-of-states-have-laws-governing-land-contracts.

- The states are Alabama, Alaska, California, Colorado, Florida, Georgia, Illinois, Indiana, Iowa, Kentucky, Maine, Maryland, Michigan, Minnesota, Missouri, Nebraska, Nevada, New Hampshire, New Mexico, New York, North Carolina, Ohio, Oregon, Pennsylvania, South Carolina, Texas, Utah, Washington, and West Virginia.

- As of this writing, the states that require sellers to record land contracts are Illinois, Iowa, Louisiana, Maine, Maryland, Nevada, North Carolina, Ohio, Oklahoma, Texas, Virginia, and Washington. Minnesota passed a bill in the spring of 2024 to require sellers to record land contracts within four months of their execution; the measure will go into effect on Aug. 1, 2024. Colorado requires that sellers notify the county assessor and treasurer—but not the recorder of deeds—about their arrangements.

- Wisconsin, Conveyances of Real Property; Recording; Titles, Ch. 706 (2016), https://docs.legis.wisconsin.gov/statutes/statutes/706/02/2.

- Pew derived its estimate of the total number of active land contracts from its 2021 nationally representative survey, which found that 0.54% of U.S. adults were actively using a land contract to finance a home purchase. Then, given that land contract buyers’ average household size is comparable to that of the country as a whole, Pew applied that percentage to the total number of households in the United States in 2022, which yielded an estimate of 689,000 households that actively use a land contract. After the survey’s margin of error is accounted for, the true number of active land contracts could be anywhere from 371,000 to 1 million. Although the relative scarcity of land contracts makes this estimate imprecise, it is nevertheless probable that many land contracts are not publicly recorded and are therefore invisible to federal, state, and local governments.

- Some Michigan land contract sellers prefer foreclosure to eviction because, although the state often requires buyers who are foreclosed on to repay their full loan balance, it requires people who are evicted only to catch up on missed payments. However, Michigan’s rules are unusual and not representative of the United States as a whole.

- National Consumer Law Center, “Summary of State Land Contract Statutes.”

- Roberto G. Quercia, Michael A. Stegman, and Walter R. Davis, “The Impact of Predatory Loan Terms on Subprime Foreclosures: The Special Case of Prepayment Penalties and Balloon Payments,” Housing Policy Debate 18, no. 2 (2007): 311-46, https://www.tandfonline.com/doi/abs/10.1080/10511482.2007.9521603.

- Consumer Financial Protection Bureau, “Consumer Financial Protection Bureau Issues Rule to Protect Consumers From Irresponsible Mortgage Lending,” news release, Jan. 10, 2013, https://www.consumerfinance.gov/about-us/newsroom/consumer-financial-protection-bureau-issues-rule-to-protect-consumers-from-irresponsible-mortgage-lending/; “What Is a Qualified Mortgage?” Consumer Financial Protection Bureau, last modified June 10, 2022, https://www.consumerfinance.gov/ask-cfpb/what-is-a-qualified-mortgage-en-1789/.

- Pew analyzed the 2022 Home Mortgage Disclosure Act mortgage data and estimated that less than 1% of mortgages are structured with balloon payments.

- National Consumer Law Center, “Summary of State Land Contract Statutes,” 25; “Residential Executory Real Estate Contracts Act,” 2019, https://lis.virginia.gov/cgi-bin/legp604.exe?191+ful+CHAP0511.

- Heather K. Way and Lucy Wood, “Contracts for Deed”; Samuel DuBois Cook Center on Social Equity at Duke University, “The Plunder of Black Wealth in Chicago,” 2019, https://socialequity.duke.edu/wp-content/uploads/2019/10/Plunder-of-Black-Wealth-in-Chicago.pdf; Sarah Mancini and Margot Saunders, “Land Installment Contracts: The Newest Wave of Predatory Home Lending Threatening Communities of Color,” National Consumer Law Center, 2017, https://www.bostonfed.org/-/media/Documents/cb/2017/spring/land-installment-contracts-the-newest-wave-of-predatory-lending-threatening-communities-of-color.pdf.

- National Consumer Law Center, “Summary of State Land Contract Statutes.”

- The Pew Charitable Trusts, “Small Mortgages Are Too Hard to Get,” 2023, https://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2023/06/small-mortgages-are-too-hard-to-get.

ADDITIONAL RESOURCES

Issue Brief