New Federal Bill Would Expand Protections for Land Contract Buyers

Impact would be most significant in states without safeguards already in place

New federal legislation would improve consumer protections for Americans who use a land contract to finance their home purchase. About 1.4 million Americans currently use land contracts, also known as “contracts for deed” or “land installment contracts,” and many report successful experiences. However, land contracts put buyers at risk of losing their homes and their investments because these arrangements lack basic consumer protections that come standard with mortgages.

Today’s land contract market is governed by a weak patchwork of state and federal laws. Only 21 states have enacted laws addressing these arrangements, and enforcement varies widely. Each year, states introduce measures to better regulate land contracts, but the legislation introduced in Congress this year marks the first time that the federal government has sought to establish minimum protections for buyers using these arrangements.

Sponsored by Senators Tina Smith (D-MN) and Cynthia Lummis (R-WY), the Preserving Pathways to Homeownership Act of 2024 would help to address some of the key risks that land contracts pose to buyers. In these transactions, the seller extends credit directly to the homebuyer, without involving a third-party lender. Unlike with a mortgage, however, land contract homebuyers obtain only equitable ownership of the property—rather than full sole ownership—until the final payment is made. This means buyers face many of the costs of homeownership without reaping its full benefits.

Even if federal legislation is enacted, additional measures will be needed to ensure that the land contract market is safe for everyone. Because of a provision that exempts sellers who have used their land-contract-financed home as a primary residence within the last two years, the bill’s safeguards do not apply to almost half of the land contract market. As a result, state lawmakers should consider enacting laws that further protect these buyers.

Federal bill would create recording requirement and expand foreclosure protection

The proposed bill targets some of the risks of land contracts through two provisions that would make these arrangements more similar to mortgages. First, the bill would require land contract sellers to publicly record their arrangements with local governments. That would guarantee that both the buyer’s and the seller’s financial interest in the property is recognized. Second, the bill would grant foreclosure protection to land contract buyers who are unable to make all necessary payments. That would ensure them the opportunity to catch up on missed payments and retain the rights to their home equity.

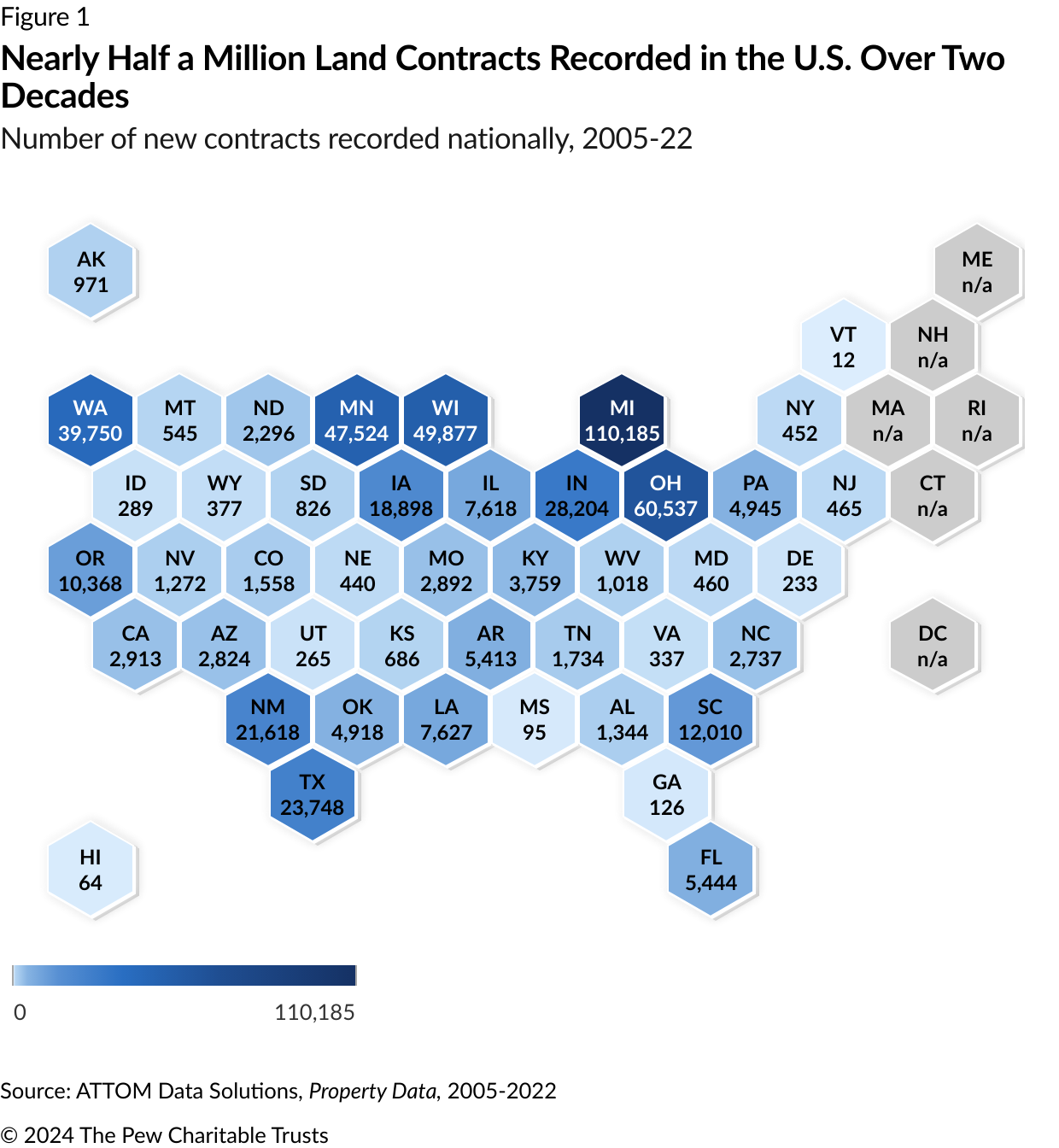

When land contracts are not recorded, buyers’ financial interest in a property is often not recognized or protected and they are often ineligible for common property tax exemptions and other government programs designed to benefit homeowners. In a nationally representative survey of land contract buyers conducted in 2022 for The Pew Charitable Trusts, just 78% of respondents indicated that their contracts were recorded. A separate analysis of property records data shows that 489,000 land contracts were recorded from 2005 to 2022, of which about 383,000 covered residential properties. (See Figure 1.) However, several states do not record any land contracts at all. The federal bill would address this by requiring sellers to record their land contracts with the local recorder of deeds office within five days of entering into the arrangement.

Although most land contract buyers report successfully repaying their arrangements, those who run into financial difficulties often do not receive the same protections as those who use a mortgage. For example, state laws are often ambiguous about whether land contract buyers are entitled to foreclosure protection, so many sellers choose to remove homebuyers using the quicker and more seller-friendly eviction process. Buyers who are evicted can be removed from their homes in days or weeks and typically do not retain the right to their home equity. The proposed federal bill clarifies that land contract buyers should instead go through a foreclosure process, which would give buyers the opportunity to catch up on missed payments or renegotiate the contract’s terms.

Most land contracts will remain unprotected, but state laws can help fill the gap

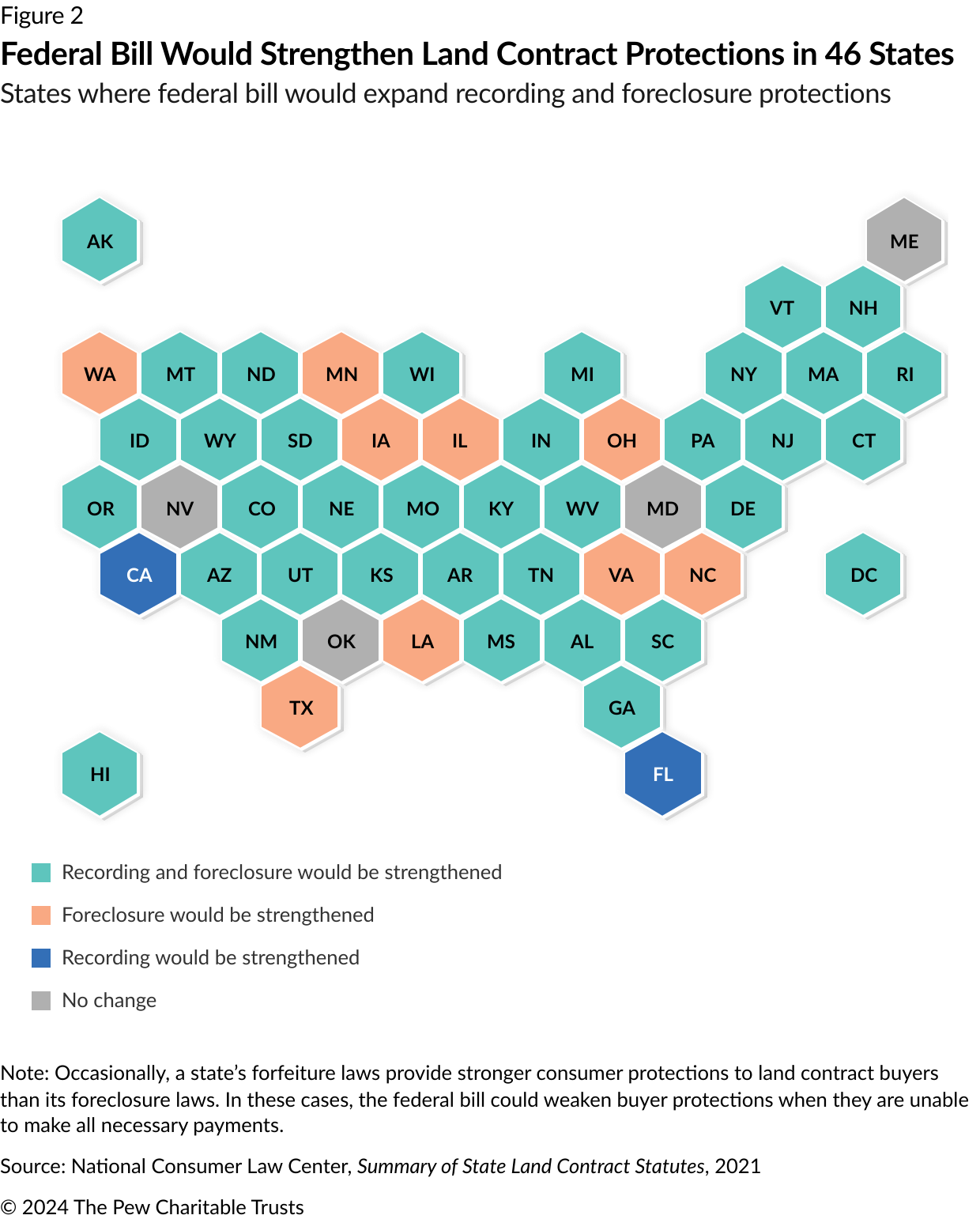

The recording and foreclosure provisions included in the Senate bill would improve protections for many land contract buyers. Still, the bill exempts land contracts used to purchase commercial, industrial, or vacant properties and also excludes home sales in which the seller has used the property as a primary residence in the preceding two years. Pew’s analysis of property records data indicates that these exemptions would exclude nearly half of residential land contracts recorded between 2005 and 2022, potentially leaving hundreds of thousands of buyers at risk.

However, the gaps in the federal bill may not be an issue everywhere because of existing state laws. Currently, 13 states have laws requiring land contracts to be recorded and six have laws that extend foreclosure protection to land contract buyers. Additionally, some municipalities have enacted laws protecting land contract buyers. Buyers in these states and localities would continue to receive the same protections they do today, as long as their jurisdiction’s land contract law exceeds the federal bill’s minimum standards.

In states without land contract laws, policymakers have an opportunity to help buyers and sellers excluded from federal protection. Although the new bill would establish minimum standards, states can introduce new protections for land contracts or extend the federal bill’s protections to a wider group of buyers and sellers.

Federal and state policymakers should consider further actions that would create uniform protections for land contract buyers. Those could include expanding recording requirements, clarifying the roles and responsibilities of buyers and sellers, and ensuring that buyers’ home equity and other financial investments are protected. Policymakers also could consider broadening protections so that they apply to rent-to-own and lease-purchase arrangements, which are often similar in structure to land contracts. Steps such as these would strengthen opportunities for safe and affordable homeownership.

Adam Staveski is a senior associate and Tara Roche is a project director with The Pew Charitable Trusts’ housing policy initiative.